AI Infrastructure: Why Are Small Labor Markets Booming?

Liz Mahon, PhD explores how data center expansion is reshaping hiring and why it's getting harder (and more expensive) to keep up.

Photo Credit: Jalen Hueser

We recently explored the macro story of Artificial Intelligence (AI). While those broader effects will take time to fully materialize, we are already seeing meaningful shifts in the geography of jobs across the U.S. A surge in investment in AI-related infrastructure (projected to reach as much as $700 billion in 2026) is fueling localized labor market booms. Notably, much of this growth is occurring in regions that were left behind by the last economic expansion.

The potential long-term upside is a more geographically distributed economy. The tradeoff, however, is emerging quickly: these regions are now experiencing acute labor shortages, creating challenges for local businesses competing with the influx of “AI money”. In this piece, we explore which occupations are benefiting most from this surge in demand and what it means for local labor markets, hiring dynamics, and recruitment costs.

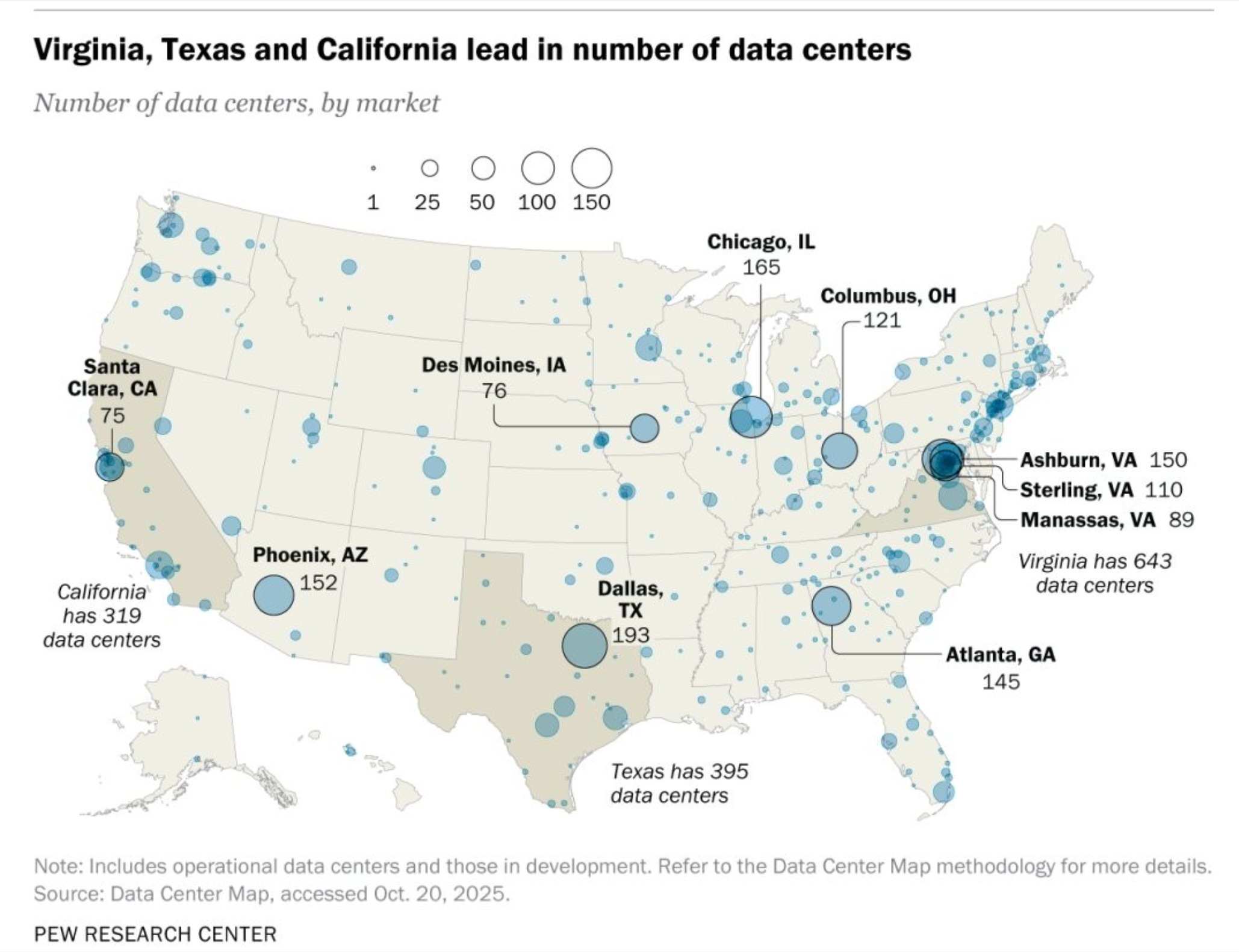

Construction of data centers is creating a job postings boom

AI is often framed as a purely digital phenomenon defined by algorithms, automation, and cloud-based systems. But this framing overlooks a critical reality: AI depends on physical infrastructure. Data centers, energy systems, cooling technologies, and the skilled labor required to build and maintain them form the foundation on which AI operates. As a result, the constraints shaping AI expansion are not just technological — they are increasingly infrastructural and labor-driven. Recent discussions of AI employment have largely focused on high-skill, white-collar roles like software engineers and data scientists, but the most immediate pressure is emerging elsewhere.

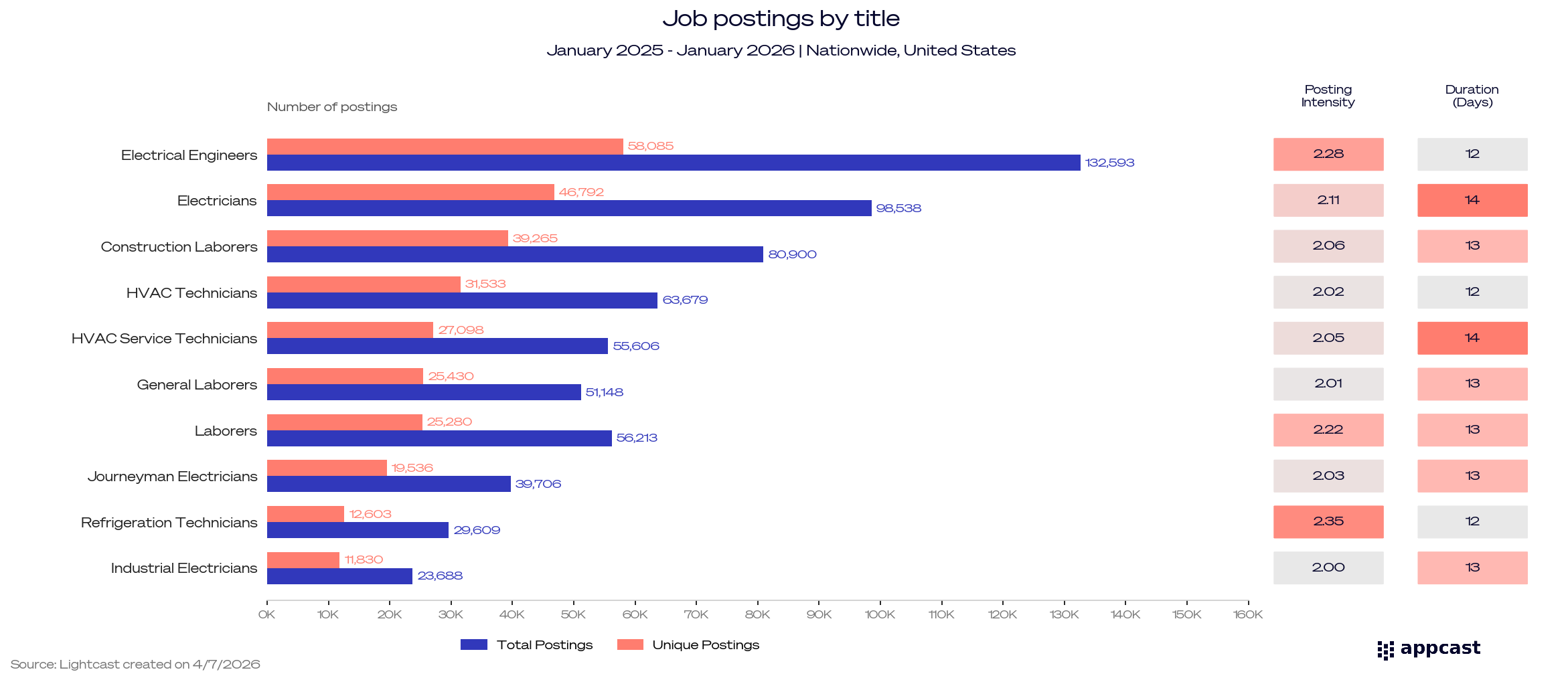

The chart below shows how hiring interest has surged across infrastructure-related roles, with electricians, HVAC (Heating, Ventilation & Air Conditioning) technicians, electrical engineers, construction workers, and industrial mechanics leading in both total and unique job postings. The far-right columns (posting intensity and duration) highlight an important dynamic: roles with higher posting intensity (which indicates how heavily employers are leaning on geographic and title expansions) and longer time-to-fill signal persistent hiring difficulty. In other words, employers aren’t just hiring more — they’re also often struggling to fill these positions.

These roles are essential to building and operating data center systems and require specialized training and certification, making them difficult to scale quickly. As a result, the availability of skilled labor has become a key limiting factor in AI expansion. This is not a marginal limitation: The U.S. is projected to face an annual shortfall of tens of thousands of electricians alone, with broader shortages across construction and technical trades.

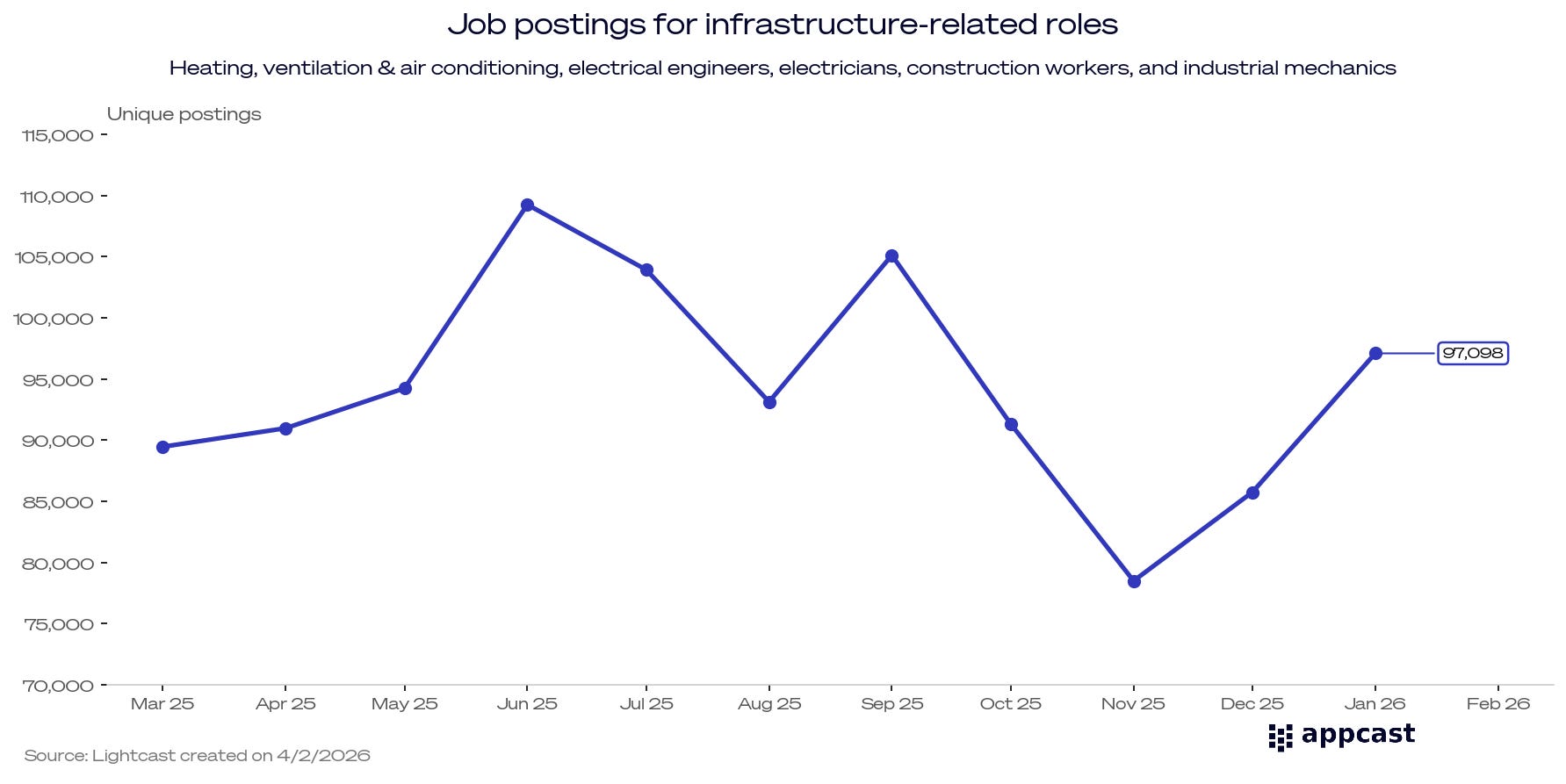

From an economic perspective, this dynamic reflects a classic demand-supply imbalance: demand is rising faster than the available workforce can respond. Data center construction spending has surged dramatically, reaching nearly $80 billion in 2025, with tens of billions more in active development. At the same time, hundreds of thousands of roles tied to this expansion remain unfilled. Instead of declining after initial spikes, job postings for these roles remain elevated, suggesting positions are taking longer to fill and talent pipelines are constrained.

This signals a broader structural issue: a shortage of workers in the occupations underpinning AI environments. Persistent job postings (especially those that remain open or are repeatedly reposted) are a strong signal of a constrained labor supply. When these patterns appear across multiple markets, they reflect systemic imbalance rather than isolated hiring challenges.

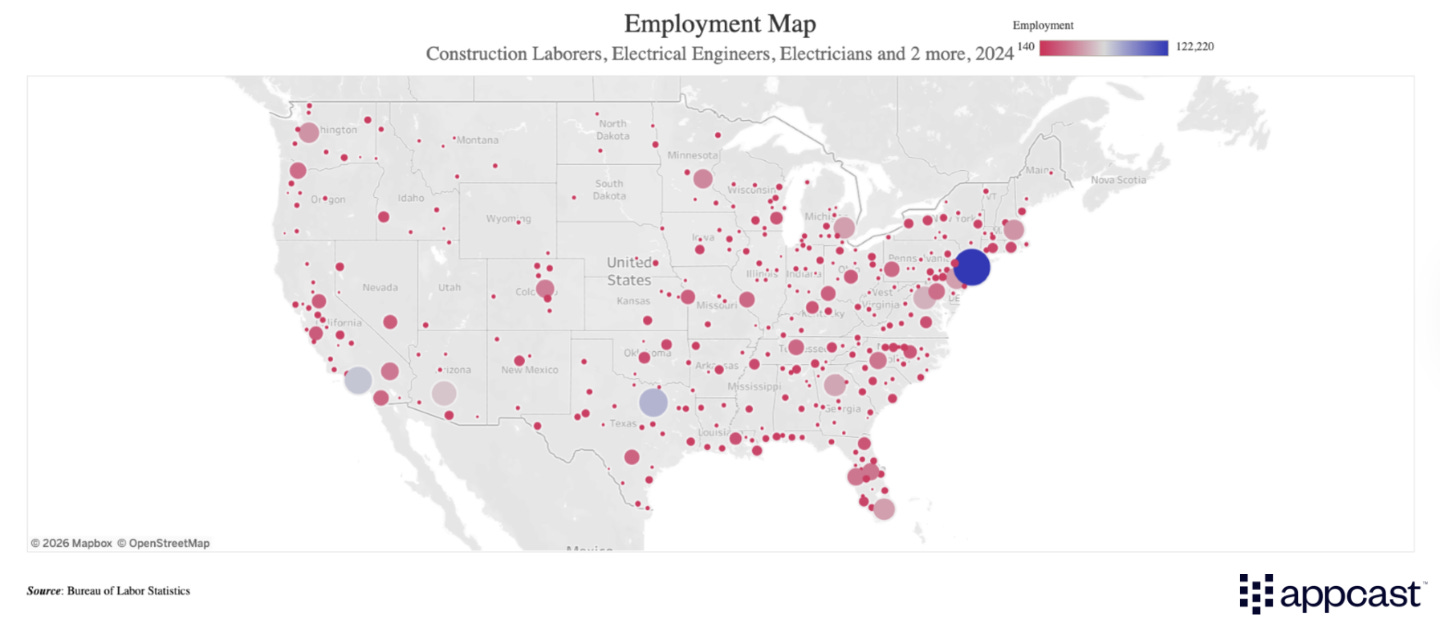

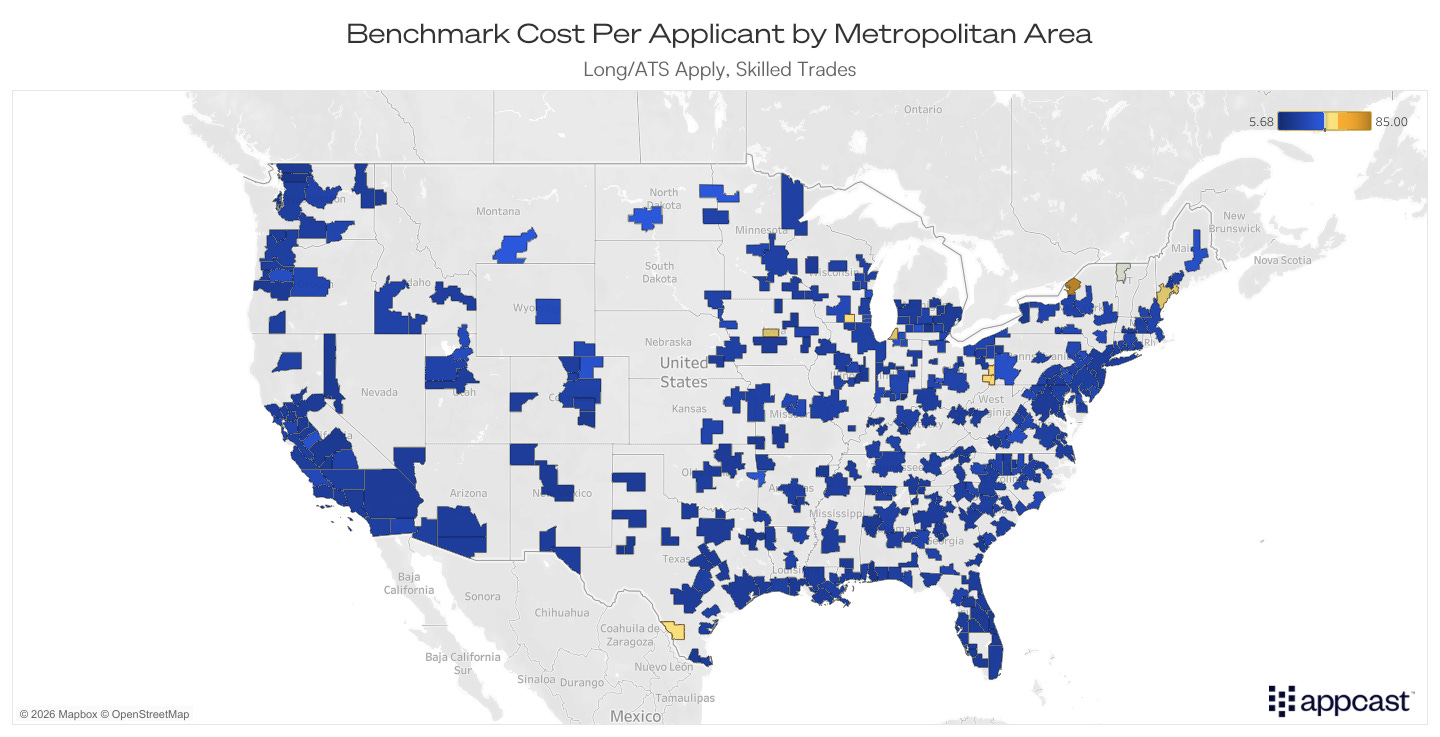

At the same time, the geography of hiring interest is shifting. The map below shows that technology employment is concentrated in a small number of major metropolitan areas. In contrast, AI architecture is expanding into smaller metros and secondary markets where labor supply is often thinner and less specialized. While this creates an opportunity to distribute economic growth more broadly, it also introduces new constraints, particularly in regions where the local workforce is not yet equipped to meet the demand.

Labor supply is not keeping pace with demand

Many of the industries experiencing increased investment in AI infrastructure have relatively small labor pools, limited training capacity, or historically lower levels of interest. As demand rises rapidly, local labor markets are struggling to keep up. This imbalance shows up in several ways, like longer time-to-fill, higher volumes of job postings, and increased competition among employers for a limited set of candidates.

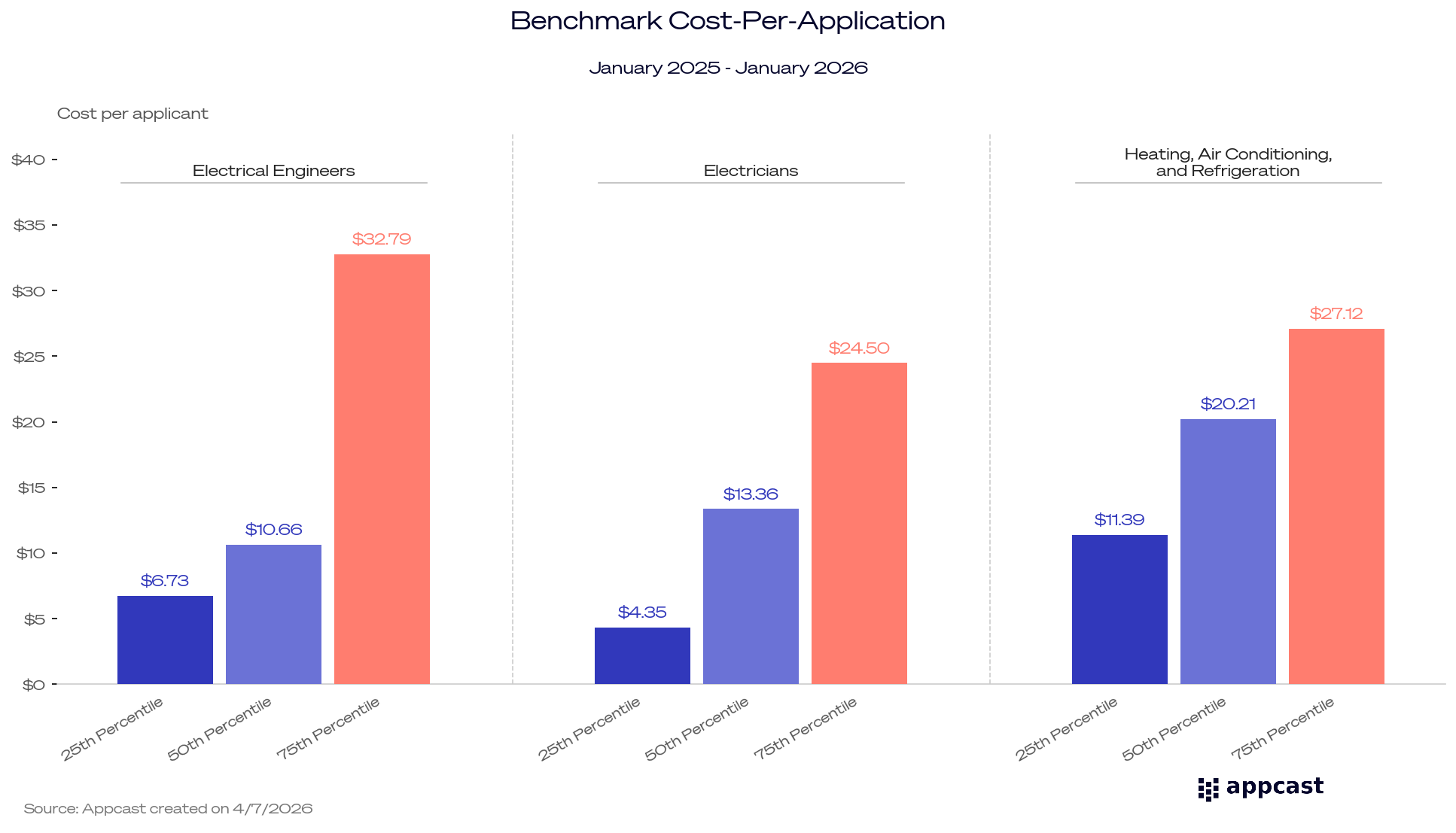

Across the U.S., hundreds of thousands of trade and infrastructure roles remain unfilled, even as demand continues to grow. At the same time, more than half of data center operators report difficulty attracting and retaining qualified workers. These constraints are often most visible in hiring costs. Cost-per-application (CPA) increases sharply at higher percentiles (especially for electrical engineers and skilled trades), reflecting intensified competition for scarce talent. As market pressure builds, employers must invest more to attract candidate attention; and in more competitive regions, CPA rises quickly as companies contend for a limited pool of qualified workers. In practice, this variation can be dramatic: some smaller or more constrained labor markets see CPA climb into the $60+ range, while major metropolitan areas like Chicago or Los Angeles can remain below $10, reflecting fundamentally different levels of competition for talent.

These dynamics are not evenly distributed. At a national level, labor market conditions may appear relatively stable, but localized analysis reveals substantial variation. Some regions remain relatively balanced, while others face acute labor shortages and significantly higher hiring costs. Increasingly, location is not just context — it is a primary driver of hiring outcomes.

What does this mean for recruiters?

AI is accelerating a redistribution of labor demand across the United States, but this shift is happening faster than the labor force can adapt. The result is a widening gap between where jobs are being created and where qualified workers are available. This is driving localized labor shortages, especially in places that weren’t previously built to support this level of demand. In some cases, this is beginning to slow the pace of AI development itself. While AI is often framed as a driver of productivity, its expansion is ultimately limited by the physical systems and workforce required to support it. The future of AI will not be determined by software alone, but by the availability of power, land, and, most critically, skilled labor.

For recruiters, this likely already feels familiar: roles taking longer to fill, rising recruitment costs for the same outcomes, and increasing variability across markets, where one region performs strongly while another struggles. This is not always a strategy problem. In many cases, it reflects the underlying reality of supply and demand. That gap is where friction emerges, but it’s also where the opportunity lies. Organizations that adapt their hiring strategies, invest in workforce development and talent pipelines, and respond to increasingly localized labor market dynamics will be better positioned to compete.

Liz Mahon, PhD is Manager of Data Analytics at Appcast, where she develops analytical strategy and leads a team of analysts in delivering data-driven recruiting solutions with an emphasis on performance optimization, data storytelling, and collaborative problem-solving. She received her PhD from Brandeis University and a BA from Harvard University. Her interests include automation development, research design, and the power of data to make the best recruiting decisions.

| A guest post by

|