Central Banks on Hawkish Standby

A breakdown of this week's central bank action — the Fed, ECB, and BoE held rates steady but signaled hikes ahead — and what the hawkish turn means for hiring.

Photo Credit: Maryna Yazbeck

We had triple central bank action this week! Despite the oil shock, the Fed, European Central Bank (ECB), and Bank of England (BoE) all decided to keep interest rates on hold. But what is notable from the monetary policy communication is how quickly the debate has changed. Oil and gas prices are already feeding back into inflation across all three geographies as the Iran war has pushed them well above pre-conflict levels (Brent is currently exceeding $110). While none of the central banks moved this round, the dissent patterns and press-conference language all point in the same hawkish direction: the next policy change will likely be a hike rather than a cut, and financial markets have adjusted accordingly.

Fed: A divided final meeting for Powell

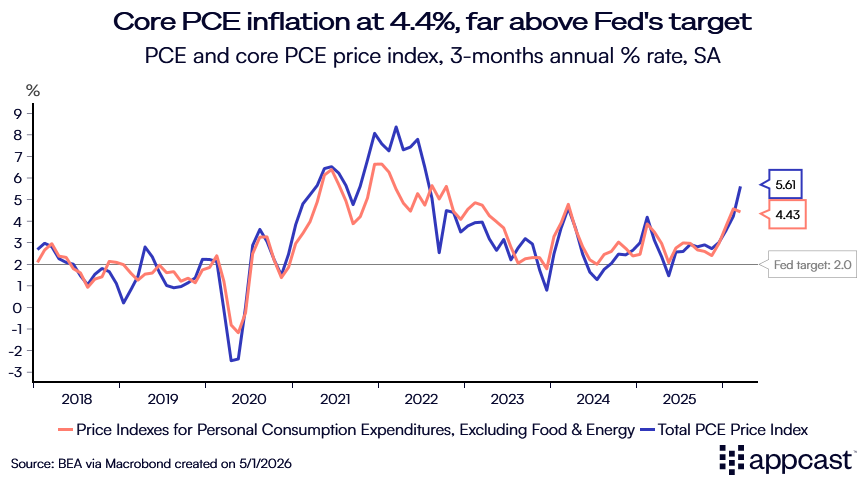

In the U.S., inflation was already accelerating and heading toward 4% before the oil shock. The tariffs imposed by the Trump administration are the main culprit, increasing the price of imported goods for American consumers.

With rising energy prices adding to inflationary pressure, the Fed decided to keep interest rates steady in its target range of 3.5%–3.75% on Wednesday. Of note, the 8–4 vote on the Federal Open Market Committee (FOMC) was the most divided Fed decision since 1992. Trump appointee Stephen Miran wanted a rate cut, while three other dissenters objected to keeping an easing bias in the statement. Financial markets read the split as hawkish, pricing in a potential rate hike by the end of the year.

This was almost certainly Powell’s last meeting as Chair of the Federal Reserve. Kevin Warsh’s nomination cleared the Senate Banking Committee the same morning, and he is expected to be confirmed in time for the June FOMC meeting. The unusual wrinkle is that Powell is staying on as a governor — his term runs until 2028 — making him the first chair since 1948 to remain on the board after stepping down from the top job. The reason: Trump’s repeated attacks threatening Federal Reserve independence. Practically, that means Warsh will chair a committee where the institutional memory — and one vote — still belongs to Powell, narrowing the room for the interest rate cuts that Trump has repeatedly pushed for.

ECB: A hawkish hold with rate hikes baked in later this year

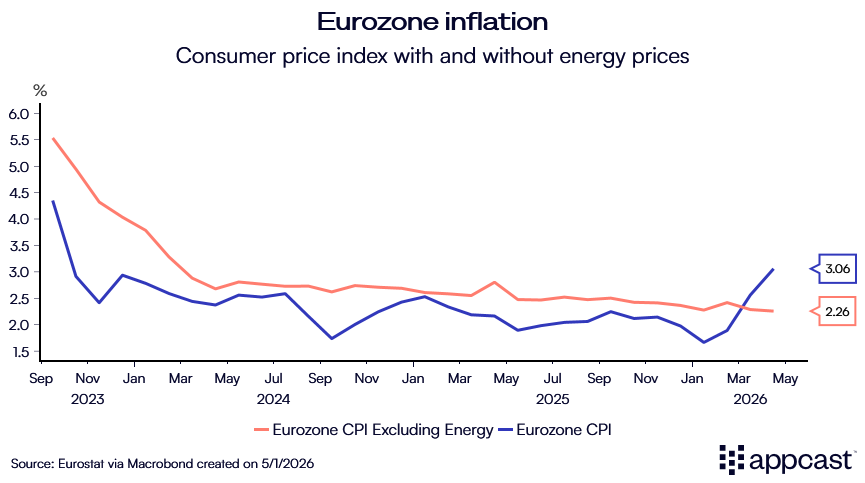

The ECB left its policy rate at 2% on the same day Eurozone inflation jumped to 3.0% — the highest level since September 2023 — with energy costs up by more than 10%.

ECB President Christine Lagarde described the decision as “an informed decision,” given that central banks face insufficient information. But with the magnitude and duration of the shock hard to pin down, much of this remains guesswork.

The ECB acknowledged that upside risks to inflation and downside risks to growth have intensified. The combination is the textbook setup for a stagflation debate, though Lagarde pushed back against that label by pointing to a still-resilient labor market in the Eurozone and domestic demand contributing to growth.

The communication, in other words, was a hawkish hold. Financial markets fully expect the ECB to hike rates in June, with at least another rate hike priced in by end of year.

BoE: Chief Economist dissents in favor of a rate hike

Inflation in the U.K. rose to 3.3% in March, driven largely by motor fuels as pump prices surged to their highest levels since 2024. Britain’s heavy gas dependence, the highest government bond yields in the G7, and a politically weakened Starmer government make the energy shock more damaging than for continental Europe.

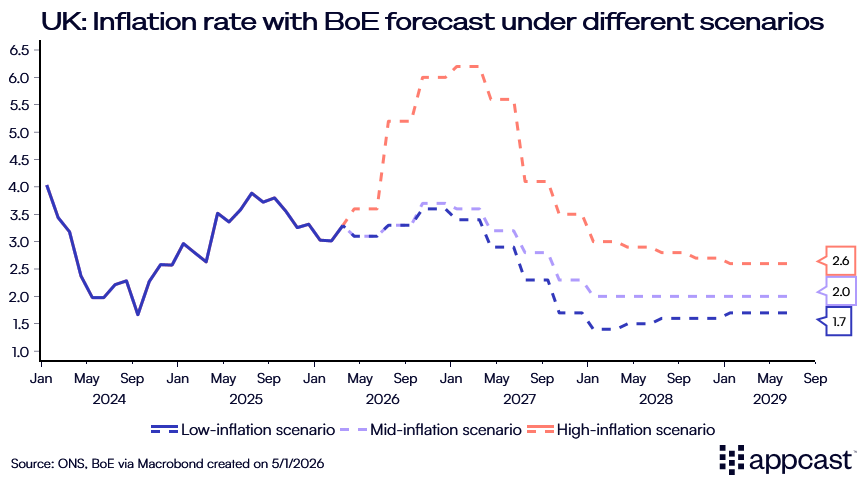

The Monetary Policy Committee (MPC) voted 8–1 to hold the policy rate at 3.75%. Notably, Chief Economist Huw Pill dissented in favor of an immediate interest rate hike. The Bank’s economic projections sketched three scenarios. The benign one has inflation reaching 3.5% before fading relatively quickly, while the most adverse has consumer prices peaking at 6.2% in early 2027 with the policy rate climbing to 5.25%.

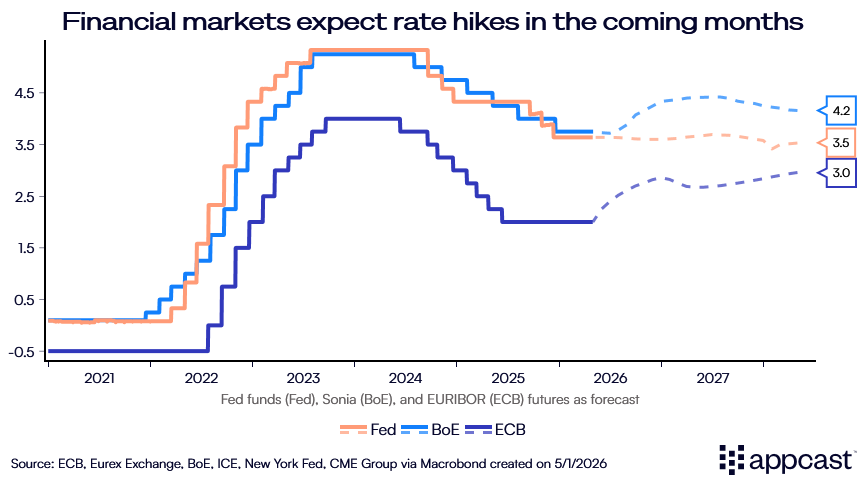

No wonder, then, that Governor Bailey also struck a hawkish tone, warning that monetary policy would need to respond if energy pass-through became “embedded and persistent.” Pre-war forecasts of two BoE rate cuts in 2026 have flipped, with financial markets now pricing in two rate hikes instead.

What does this mean for recruiters?

Our recent piece laid out three channels through which the Iran oil shock feeds into hiring: a direct hit to household discretionary income, a profit-margin squeeze for businesses, and a monetary-policy tightening that piles on top. This week’s meetings make it clear that the third channel is no longer hypothetical. The Fed, ECB, and BoE have all moved from “we will likely ease policy” to “the next move is probably up.” Financial markets are reacting accordingly: government bond yields have surged, and credit is getting more expensive for households and businesses alike.

For recruiters, the practical implication is that rate-sensitive sectors — construction, real estate, manufacturing — face a double whammy of weaker demand and higher financing costs at exactly the moment central banks are signaling they will lean hawkish rather than rescue them. Hospitality and retail will feel the consumer-spending pullback. Healthcare, education, and the public sector remain the most insulated, as they typically are in this kind of cycle.

The U.K. economy is the canary in the coal mine: the BoE’s own adverse scenario has interest rates climbing to 5.25%. With Britain’s high energy exposure and bond-market vulnerability, the labor market could weaken faster there than in the U.S. or Eurozone. This isn’t a recession call yet, but recruiters should prepare for a rough period of higher inflation and lower growth across advanced economies. Hiring plans for the back half of 2026 need to be built around that.