Jobs Day, December 2025

Economist Sam Kuhn dissects the last jobs report of 2025, suggesting that hiring is weakening even after accounting for DOGE and immigration restrictions.

Welcome to Recruitonomics’ first Substack post! Going forward, all posts on the former Recruitionomics.com site will now live on Substack. We will continue our normal U.S. jobs day coverage from myself and Chief Economist Andrew Flowers, as well as international coverage from Senior Economist Julius Probst.

Photo Credit: Sean Pollock

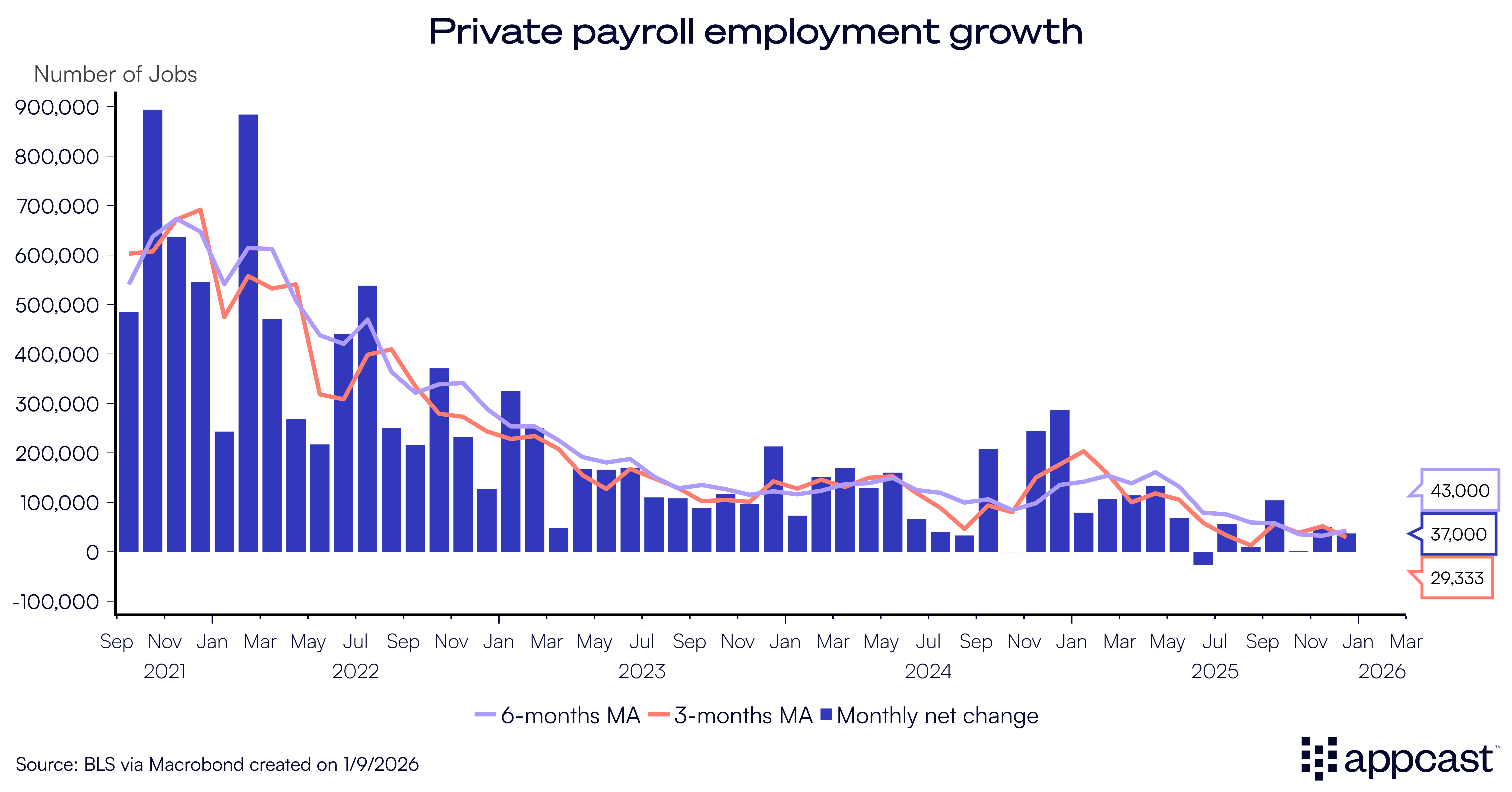

The final jobs report of 2025 showed a continuation of trends from the previous eight months: moderating job growth concentrated in healthcare and subtle warning signs of a struggling job seeker. Overall job growth rose by 51,000 in December but over a three-month average declined by 22,000, largely the result of DOGE cuts. The unemployment rate fell modestly to 4.4%, which can partly be explained by statistical wonkiness from the shutdown.

Yet, removing the effects of the shutdown and deferred resignations, private payroll growth is growing at just 29,000 over a three-month average — less than half the pace of the pre-Liberation Day trend. Policy uncertainty and restricted immigration explain most (though not all) of the recent decline in job growth.

After accounting for DOGE cuts and labor supply, private payroll growth weakened throughout 2025 as hiring appetites diminished. 2025 was a year marked by uncertainty. When government policy rapidly shifts, often businesses hold back on hiring and investment decisions. Reflecting on the years’ worth of data, it’s clear that most sectors across the labor market slowed hiring.

Industry Breakdown

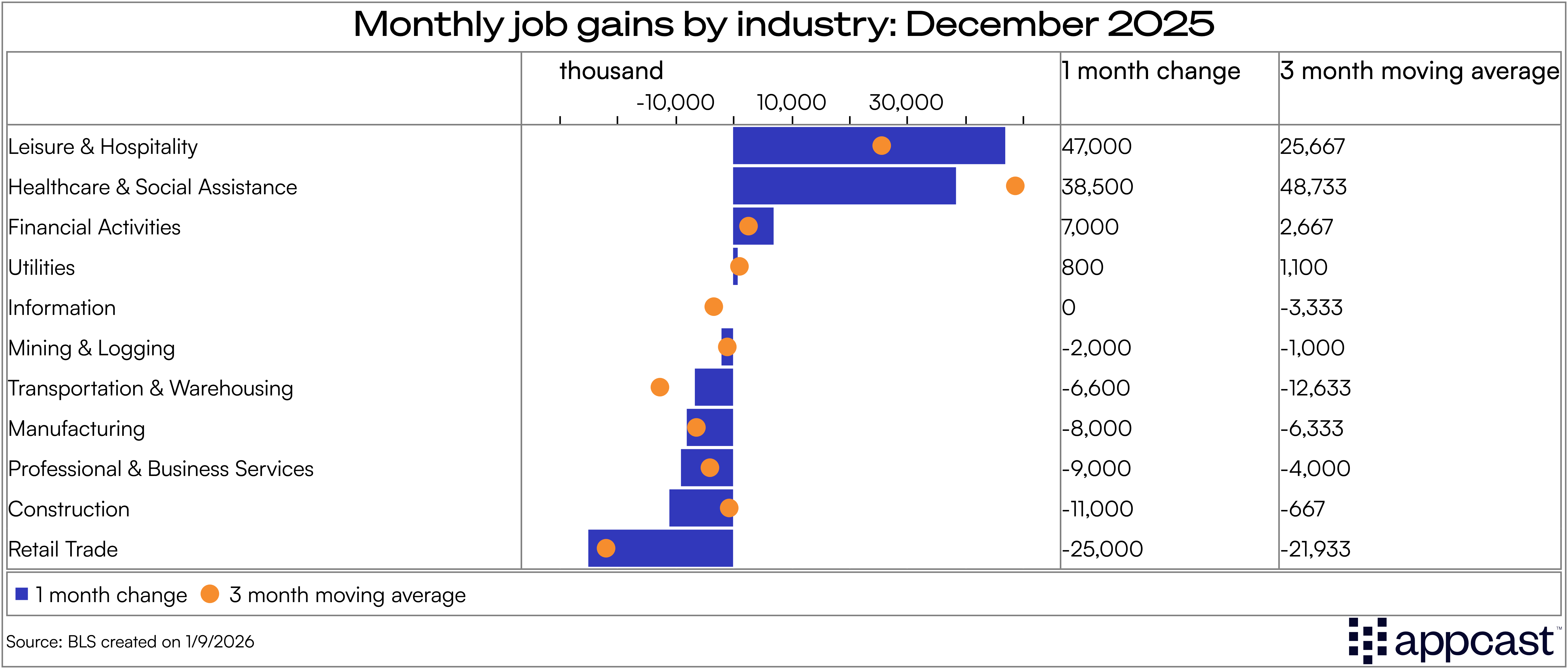

By sector, healthcare & social assistance was the main contributor to growth in 2025 — but it ended the year with its lowest contribution yet, adding just 38,500 jobs. The house passed an extension of ACA subsidies yesterday, a major headwind for healthcare hiring in 2026 as millions were at-risk of higher insurance premiums.

Goods-oriented sectors struggled in 2025: manufacturing employment declined 68,000 in 2025; likewise, transportation & warehousing declined by 79,800 jobs. Industries sensitive to trade policy felt harsher impact than service-oriented sectors like hospitality and healthcare.

Earlier this year, I published a blog on what seasonal retail hiring may look like in the fall of 2025, predicting lower retail hiring demand than years prior. The retail sector lost 25,000 jobs in December (seasonally adjusted), yet the three-month trend in job growth is positive at 9,000. Compared to 2024, seasonal hiring was modestly higher in 2025 but still below the pace earlier in the 2020s.

The tech industry, and more broadly white-collar hiring, struggled immensely in 2025. Both the Information sector (-26k) and Professional & Business Services (-62k) reduced employment in 2025. Elevated interest rates from 2023 onwards have weighed heavily on these industries, but several rate cuts by the Fed in 2025 may open a path towards modest growth in the new year.

Labor Force Insights

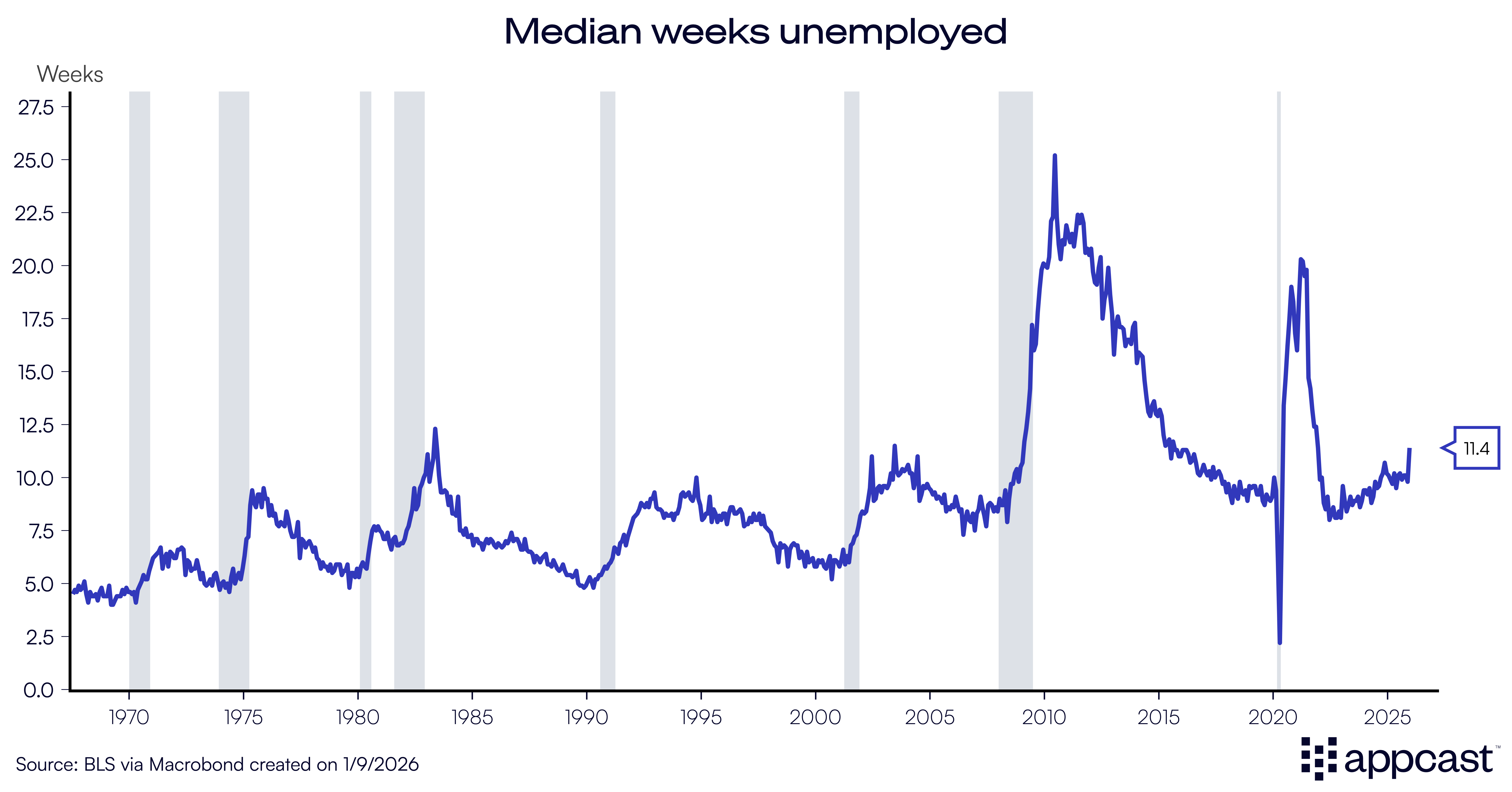

Job seekers are clearly struggling in this labor market: the median number of weeks a worker is unemployed rose sharply to 11.4, its highest point in nine years. Some of this may be explained by the government shutdown, yet its clear workers are taking longer to find new jobs. The increasing length of unemployment is concentrated in long-term unemployment, as both workers who were unemployed 15 to 26 weeks and 27 or more weeks steadily crept up.

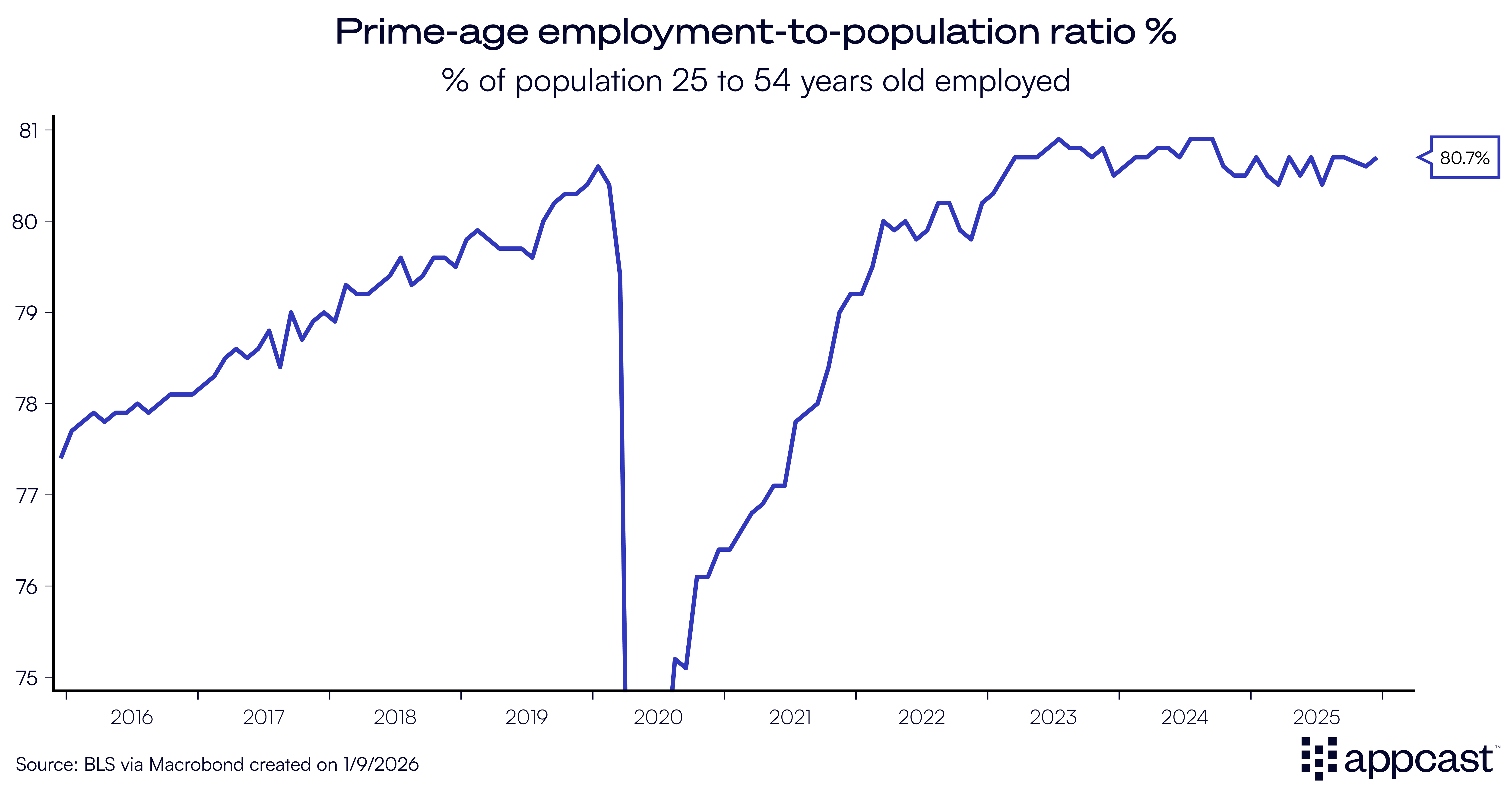

Despite cracks in the margins of the labor market, the core remains intact. The prime-age employment-to-population ratio (the percentage of the population aged 25-54 who are currently working) is still 80.7%, a near-high for the cycle and a positive sign. Outside of that group, the unemployment rate for younger workers rose steadily to above 10% in 2025.

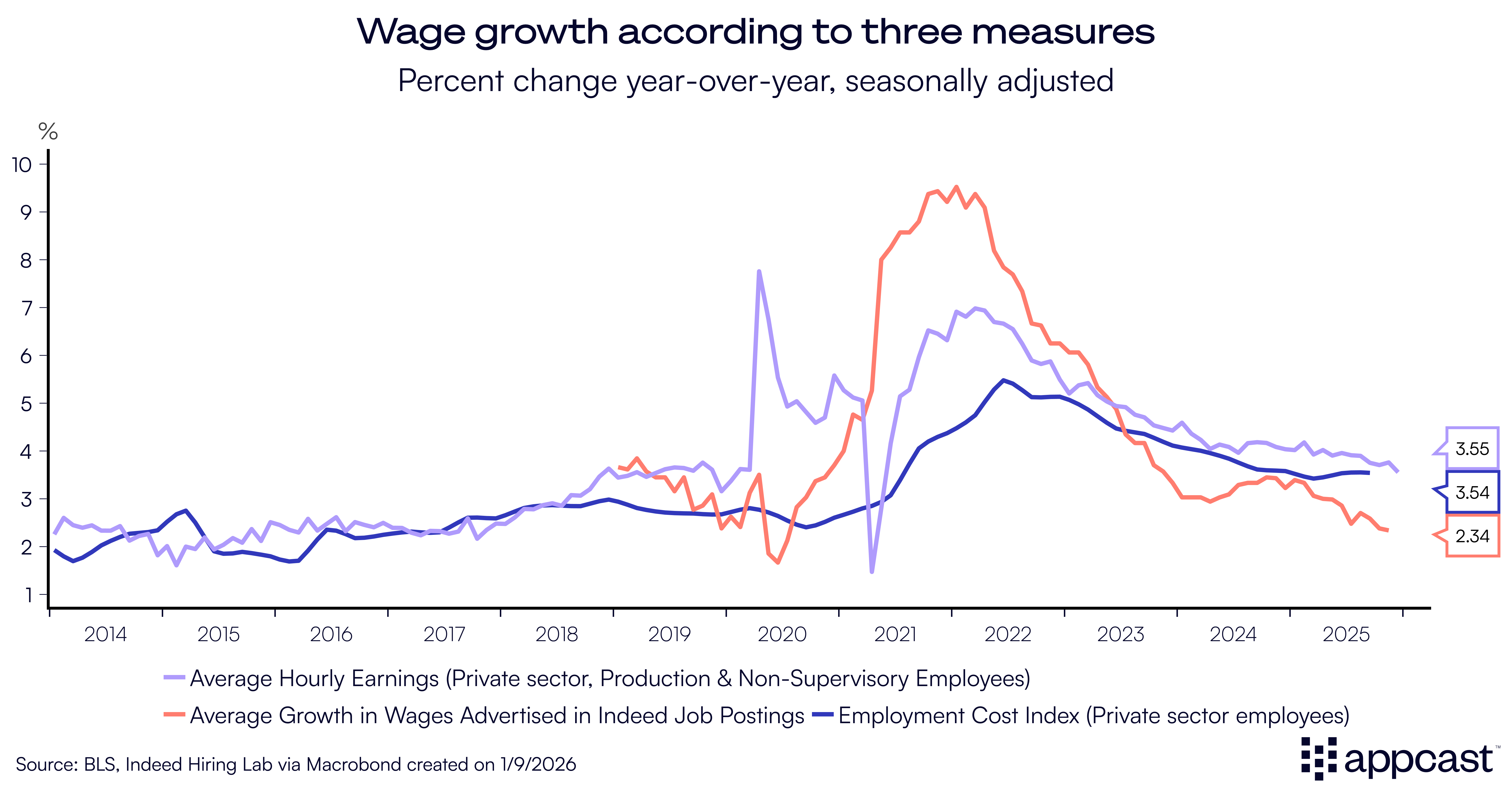

As hiring demand has cooled, so has wage growth. Average hourly earnings growth for private-sector non-supervisory workers ticked down to 3.6%, its lowest reading in the post-pandemic recovery. Other measures of earnings growth tell a similar story: advertised wages on Indeed are growing at just 2.3%, while the Employment Cost Index grew at 3.5% in Q3 of 2025.

What does this mean for recruiters?

Job growth slowed in 2025. That picture is muddled by several factors: a sharp drop in Federal Government employment from DOGE cuts, lower labor supply due to immigration restrictions and post-liberation day trade policy uncertainty.

Taking these forces into account, the labor market is in its weakest state in the post-pandemic recovery. Yet, broader economic growth according to GDP is rip-roaring. Perhaps businesses and workers have become more productive post-AI boom, reducing hiring needs.

For recruiters in healthcare and other service-oriented sectors like restaurants, hiring demand will likely persist in the new year. For recruiters in goods-oriented sectors, the picture is mixed. The Supreme Court will imminently issue a decision on Presidential tariff authority, which may radically shift the outlook going into 2026. Data center construction may continue to be a tailwind for skilled trades hiring.