Wage Pain: Workers Are Losing to Inflation, Again

Julius Probst, PhD, breaks down how the oil shock is wiping out real wage grains across the U.S., U.K., and Eurozone — and what it means for talent attraction.

Photo credit: Markus Winkler

The inflationary surge following the pandemic was extremely painful for workers. Wages failed to keep up with prices when inflation rose to nearly 9% in the U.S. and more than 10% in Europe in 2022. It took the average employee several years to gain back their lost purchasing power. Due to the oil shock this year, inflation has already surged above wage growth again within a couple months. Even with a quick resolution of the conflict, the inflationary legacy of the war will remain with us for the rest of the year, if not longer.

Workers’ confidence in the job market is already at a record low as fears of AI displacement have spread, while the economy remains stuck in a low-hire, low-fire equilibrium. Yet another cost-of-living crisis is exacerbating worker discontent around the world. Unlike a few years ago when wage demands soared, workers’ bargaining power has been reduced by today’s low-churn labor market. If the oil shock drags out, wage growth might run below inflation until early 2027.

US: Two lost years of real wage growth

Inflation in the U.S. surged during the post-pandemic economic recovery to just over 8%. This was due to a combination of several factors: a very hot economy and labor market together with supply chain disruption and an energy crisis caused by the war in Ukraine. The inflation rate was well above nominal wage growth throughout 2021 and 2022, meaning that workers were losing ground at the time. From 2023 onward, inflation fell fast enough for real wages to recover and start growing again.

But all of that changed with the conflict in Iran, which has created another global energy price shock. With U.S. consumer prices quickly accelerating from about 2.4% in February to 4.2% in May, real wages have already fallen by more than 1% within months. Most forecasts anticipate that the U.S. Consumer Price Index (CPI) will remain just under 4% in the third quarter before slowly falling back to 3.5% in early 2027. If nominal wages continue to grow at their current rate of 3.5% — assuming no further labor market slowdown — American workers will see their paychecks erode until next year. Under that scenario, real wages in March 2027 will not be higher than in July 2025, meaning more than 18 months of stagnant pay in real terms.

UK: Real wages still above water but plunging fast

Nominal wage growth in the U.K. has proven to be remarkably sticky even as the labor market went from hot in 2022 to ice-cold more recently. Supply-side imbalances caused by Brexit, the rising minimum wage, and elevated wage demands are potential explanations. Either way, nominal wage growth has only slowed to about 4% this year, while inflation has been running at a lower rate since 2023. Consequently, workers in Britain have been able to claw back some of the purchasing power they lost during the inflationary spike a few years ago.

But inflation is now heading toward 4% in the U.K. as well. Meanwhile, the Bank of England expects wage growth to fall below 3.5% due to the sluggish labor market. As a result, real wages are expected to fall by more than 1% relative to where they were before the oil shock. A reasonable projection is that they won’t recover until March 2027, implying more than a year of purchasing power stagnation for the average British worker.

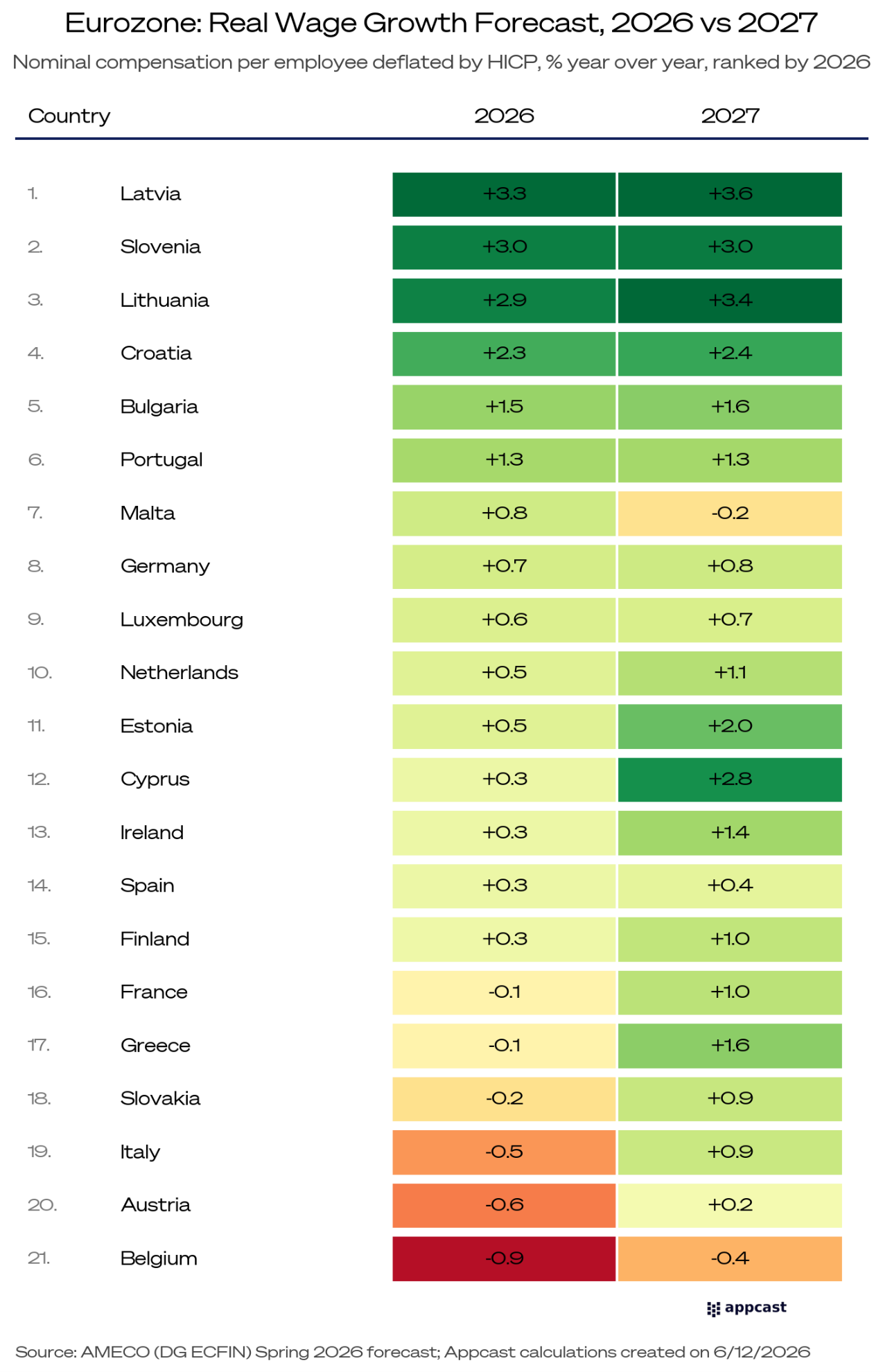

Eurozone: Real wages barely higher than in 2019

The decline in real wages in the Eurozone will most likely be somewhat smaller as inflation remains more contained than in the U.K. or U.S. Nominal wages are expected to grow at a rate of a little over 3%, while inflation will rise to 3.5% later this year. Nevertheless, real wages in March 2027 will still be slightly lower than they were in fourth quarter of last year. What’s even more concerning is that real wages a year from now will barely be higher than in early 2022, implying four years of stagnation. The reason, of course, is that it took about three years to recover from the massive stagflationary shock caused by the war in Ukraine.

Some Eurozone economies are doing better than others

While most Eurozone economies will see almost no real wage gains in the year to come, some countries are weathering the shock better than others. Economic growth in the Baltics and parts of Southern Europe — Croatia and Slovenia — has been quite spectacular in recent years, far exceeding the Eurozone’s average. As a result, nominal wage growth remains extremely high, well above 6%. Even with inflation approaching 4%, real wages continue to perform strongly in those countries, growing at a rate of 2% or 3% this year. In large Eurozone economies, on the other hand, workers will see their pay barely keep up with inflation.

What does this mean for recruiters?

While the memory of the cost-of-living crisis from a couple of years ago is still fresh, advanced economies are now facing another stagflationary shock — meaning higher inflation and lower growth. Even with a quick end to the conflict, inflation is expected to remain higher for longer. Real wages in most advanced economies are already falling, and it will take another year for them to recover to pre-crisis levels. Even as workers are bearing the brunt of the burden, it’s also bad news for companies. In the current economic environment, many employers might fail to adjust wages in line with rising living costs. With worker discontent inevitably rising, productivity will suffer. But bad morale is not the only thing that company executives will have to worry about. Talent attraction might also become more challenging. With elevated economic uncertainty and rising inflation, workers will be more hesitant to switch jobs unless there is a reasonable pay uplift relative to what they currently earn. Companies face a bind: margins are squeezed by the same inflation hitting their staff, yet persuading candidates to leave their existing roles now costs noticeably more than it did two years ago. For recruiters, that means a year of difficult conversations with both candidates and hiring managers, with neither side likely to budge easily on pay.