A Reassuringly Solid Jobs Report Bucks Conventional Wisdom

Andrew Flowers and Julius Probst, PhD dissect the latest US jobs report, which defied labor market skeptics with stronger-than-expected job gains.

Photo Credit: Brian Stalter

The consensus view of the U.S. labor market is that job growth is slowing, both because of weaker employer demand and declines in labor supply thanks to immigration restrictions. The April jobs report offers tentative signals that may defy that simple narrative.

Employment growth defies the skeptics

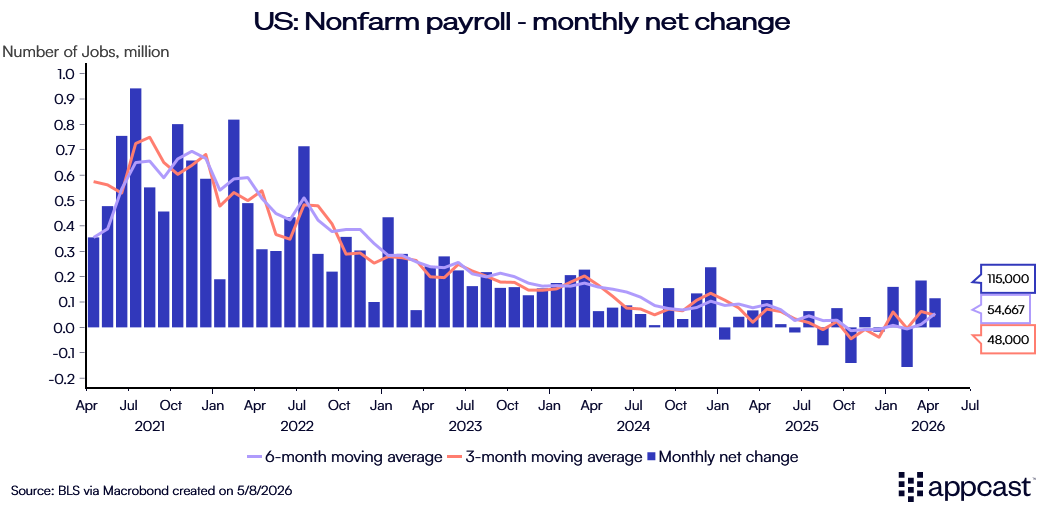

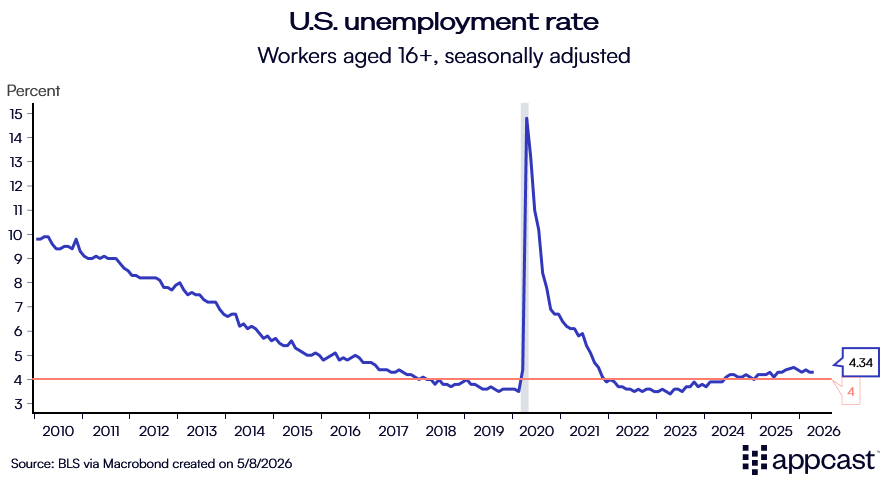

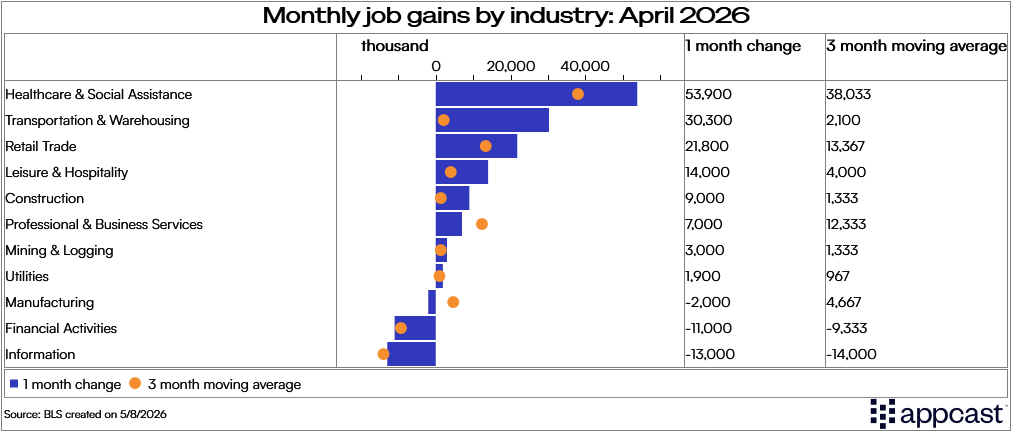

On the surface, the report was reassuringly solid: 115,000 jobs added (well above the median forecast) and the unemployment rate held steady at 4.3%. Healthcare and social assistance once again led all sectors in job growth, adding 54,000 jobs. Wage growth for all private employees was 3.6% year-over-year — a slight miss on the soft side. So far, all seems normal.

Where the report bucks conventional wisdom is that the underlying pace of private-sector job growth — now at 68,000 per month, over the six months through April — the highest in 12 months. This exceeds the so-called “break-even” rate economists have estimated based on changing demographics. And despite the stronger-than-expected job gains, the actual unemployment rate (un-rounded) increased slightly, from 4.26% to 4.34%. As pointed out by Greg Ip, this defies the narrative: if job growth is so strong, and restricted immigration is (presumably) reducing labor force growth, then the unemployment rate should be going down.

The most likely explanation is that the opposite is happening on the labor supply side. Rather than shrinking, the pool of available workers appears to be growing. More people looking for work — not fewer jobs being created — is what’s nudging the unemployment rate up.

Jobs are spreading beyond healthcare

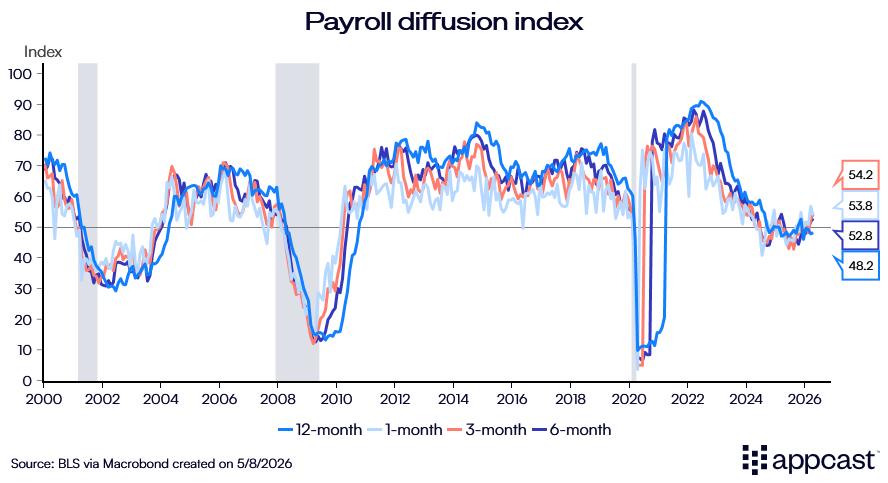

Moreover, the breadth of job gains has recovered from its low points over the past six months. The diffusion index, which measures what share of industries are adding jobs compared to those contracting, has been trending upward on a 3- and 6-month basis. The 1-month index is also up materially from six months ago (53.8 in April 2026, compared to 48.6 in October 2025).

This tells us that a labor market which once was only adding healthcare jobs is now just mostly adding healthcare jobs.

Retail has seen a pickup in job gains over the three months through April, adding roughly 13,000 per month; ditto for white-collar jobs in professional and business services, up about 12,000 a month. Transportation and warehousing, long subdued due to tariffs and associated uncertainty, added a whopping 30,000 jobs in April. This surge is unexpected.

What does this mean for recruiters?

All this to say: this wasn’t just a better-than-expected jobs report. The expected oil shock effect from the Iran war is not really showing up (yet, if ever). The April jobs report offered early, tentative signs that job growth may be more broad-based than at any point in the last year, and that labor supply isn’t as great of a chokepoint as we thought.

For recruiters, that broadening matters. Hiring demand is no longer concentrated in healthcare alone, and more sectors are quietly coming back online. By no means is this a jobs boom — far from it — but it does provide evidence of labor market stability. That stability, combined with worrisome inflation readings, suggests the Fed is more likely to remain biased toward holding interest rates steady, if not possibly hike in the future.