Stop Freaking Out About the Falling Labor Share

Julius Probst, PhD explains why the much-feared collapse in workers' share of the economy is largely a mirage created by incomplete data.

Photo credit: Alexander Grey

Well, maybe you weren’t worried about the falling labor share. But some people are — and they probably shouldn’t be. I’ll explain why.

Wage angst

There is no doubt that the emergence of AI has created a lot of anxiety among workers. And for good reason: the technology will certainly change the labor market quite dramatically in the decade to come. While we do not believe that a doomsday scenario involving mass unemployment and collapsing economic output is realistic, AI will create winners and losers as it becomes more deeply integrated into the production process. Routine white-collar workers are at risk of displacement, while AI knowledge workers stand to gain.

Alongside fears of technological unemployment, concern about the collapsing labor share — the portion of GDP that goes to worker compensation — has been circulating. As AI displaces workers and boosts profits, wages are being squeezed, the argument goes.

While the raw data seems to support this story, it’s largely a methodological issue. Once the necessary adjustments are made, the share of economy-wide income paid out to workers has remained more stable.

Profits up, wages down?

On the surface, it certainly looks like workers are losing out. The measure of the labor share from the Bureau of Economic Analysis (BEA) shows that more than 60% of GDP accrued to workers a few decades ago. More recently, that figure has dropped below 54%. Meanwhile, corporate profits have risen to an all-time high of 14% of GDP, about 4 percentage points above their long-term average. Thus, the popular narrative is that profits are eating into wages.

However, this is a gross simplification (read on and you might catch the pun). When the necessary adjustments are made, the data shows that workers are not significantly worse off.

What are imputations and why are they part of GDP?

Gross Domestic Product (GDP) measures the total value of all goods and services produced in the economy over the course of a year.

However, each year, capital gets used up: machines wear out, software becomes obsolete, buildings deteriorate. As a result, a portion of total production must be diverted to replace worn-out capital (this is called depreciation). It should be clear that this money goes neither to capital owners as profits nor to workers in the form of wages. It simply keeps the capital stock in the economy intact.

What is interesting is that depreciation has markedly accelerated in recent decades, rising from about 12% of GDP in the 1960s to more than 16% today.

Part of the reason lies in today’s internet economy. Equipment such as computers, smartphones, and software becomes obsolete significantly faster than traditional manufacturing machinery.

Another factor we need to account for is imputed rent — the hypothetical rent a homeowner would pay to themselves.

Why do economists include this “made-up income” in GDP?

Well, think of two economies: a nation of renters — Germany — and a nation of homeowners — the United States. Now imagine that in Germany, I live in your house while you live in mine, and we each pay rent to the other. This rental income is counted as part of Germany’s GDP. But in the U.S., we live in our own houses, so no rent is actually paid. As a result, Germany’s GDP would appear artificially higher relative to the U.S., even if the underlying level of economic productivity were the same — unless we include imputed rent in the U.S. GDP figure!

Given that the housing market has become more expensive over time, imputed rent has risen from about 5% of GDP in the 1950s to more than 8% today.

Both depreciation and imputed rent have surged, but this portion of economic output is neither wage nor capital income. We therefore need to deduct them from GDP to get a more accurate picture of whether workers are truly losing out. And that’s not all: we also need to account for proprietors’ income.

What is proprietors’ income?

This is money earned by people who own and operate unincorporated businesses — sole proprietorships, partnerships, and the like. It therefore measures income of the self-employed.

In the 1950s, 40% of proprietors’ income came from agriculture, but that has fallen to under 4% in recent years. Today, we are mostly talking about gig workers (think Uber), freelancers (professionals like consultants), self-employed medical practices (dentists), and family-owned businesses.

What’s problematic about this measure is that we cannot know for sure how much of the income is derived from labor vs. capital. Think about a self-employed dentist making $300,000 a year. How much of the earnings are derived from skill, and how much comes from the equipment and facilities used in the practice? Hard to say!

Historically, economists have assumed that the wage-capital split is roughly 60-40. However, that might not be quite right anymore since self-employment has become more “labor-intensive” over time. While farms are capital-intensive (lots of machinery), a self-employed consultant may rely on little more than a laptop and a phone.

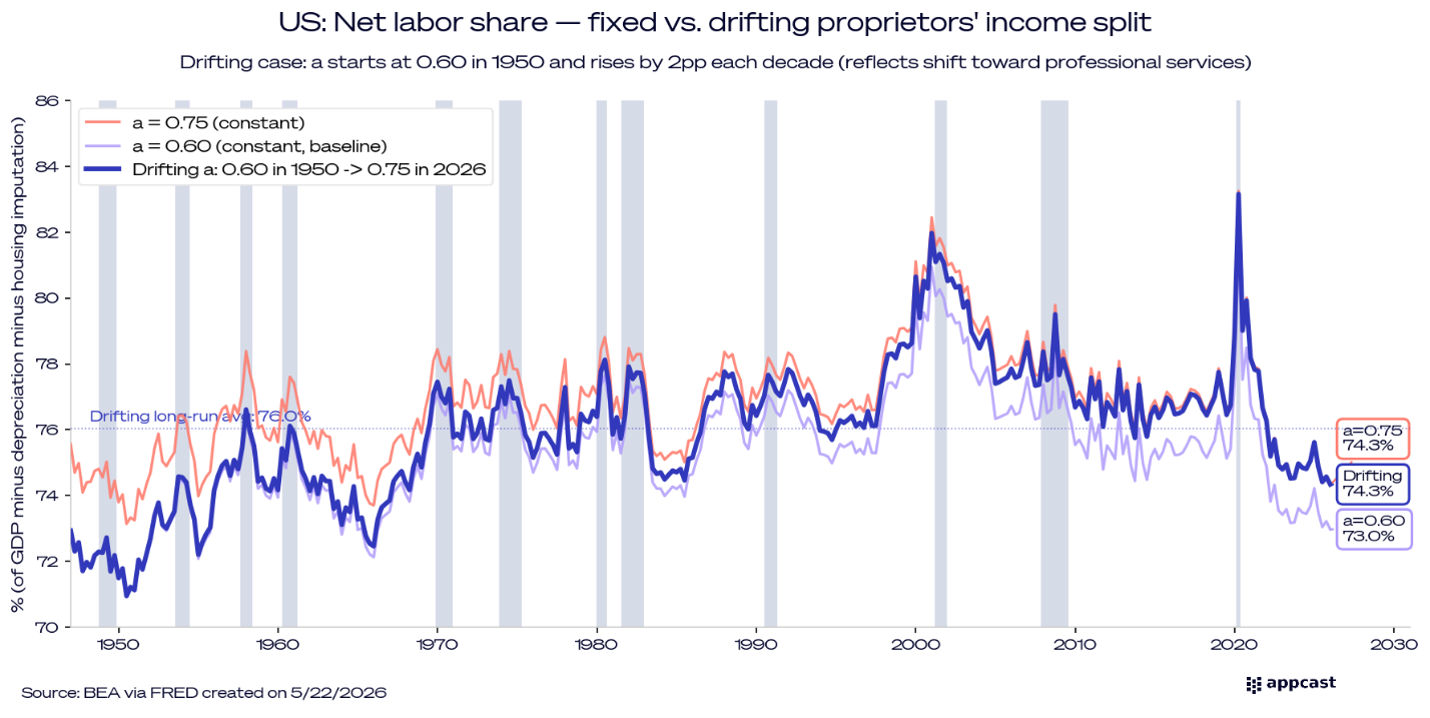

I have therefore used three assumptions for the labor share of proprietors’ income:

60%

75%

A drifting share (starting at 60% in the 1950s, and increasing by 2 percentage points each decade, slightly exceeding 75% today)

Given how the nature of self-employment has changed over time, the last scenario strikes me as the most plausible. The data shows that the labor component of self-employment has increased by more than 1 percentage point in recent decades, from about 4% in the 90s to more than 5% today.

Focus on the net labor share

Given all the considerations mentioned above, we need to focus on the net labor share — the portion of economy-wide income that goes to wages when deducting depreciation and imputed rent from GDP:

The dark blue line in the graph below shows how the net labor share has evolved over time. It is higher than in the 1950s and 1960s, and slightly lower than in the 2000s and 2010s. The 1.5 percentage point decline over the last decade is real, but significantly lower than what doomsayers would suggest!

Households are also capital owners

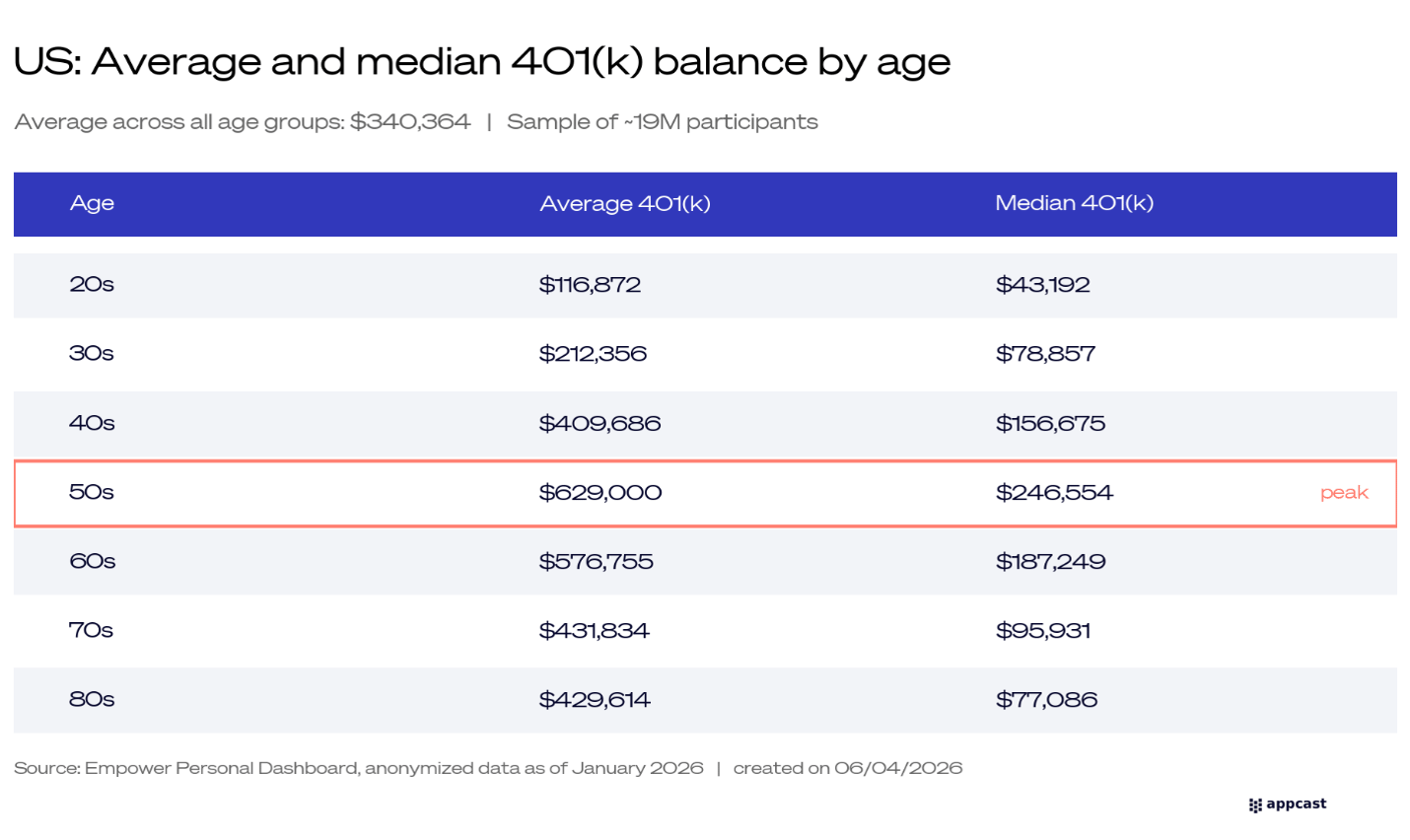

Another thing worth mentioning is that capital income does not just consist of corporate profits. While the gains have been unequally distributed, workers have been participating in the asset price boom of recent decades. This is true not just true housing but also for stocks. According to data from Empower — a U.S. retirement plan administrator with roughly 19 million participants — the median 401(k) for workers in their 50s is about $250,000, while the average is close to $630,000. While contributing members skew toward higher-income earners, the broader trend still holds: many workers have benefited from rising stock markets. This means the typical worker is not just a wage earner but also a capital owner. Moreover, new research shows that gains from stock-based compensation are not captured in standard labor income measures either.

Summing up

The gross labor share is an inadequate measure to assess whether workers are being squeezed. The main reason is that imputations — depreciation and imputed rent — make up a much bigger slice of GDP today than they used to.

While these “non-existent cash flows” represent real economic activity, they are not part of either labor or capital income. To get a sense of whether workers are losing out relative to capital owners, we need to add proprietors’ wage income and deduct the imputations from GDP. This measure — the net labor share — has fallen by roughly 1.5 to 3 percentage points since 2010.

So, while it is true that the share of income going to workers has declined slightly, the overall narrative has been exaggerated by a misleading interpretation of the data!